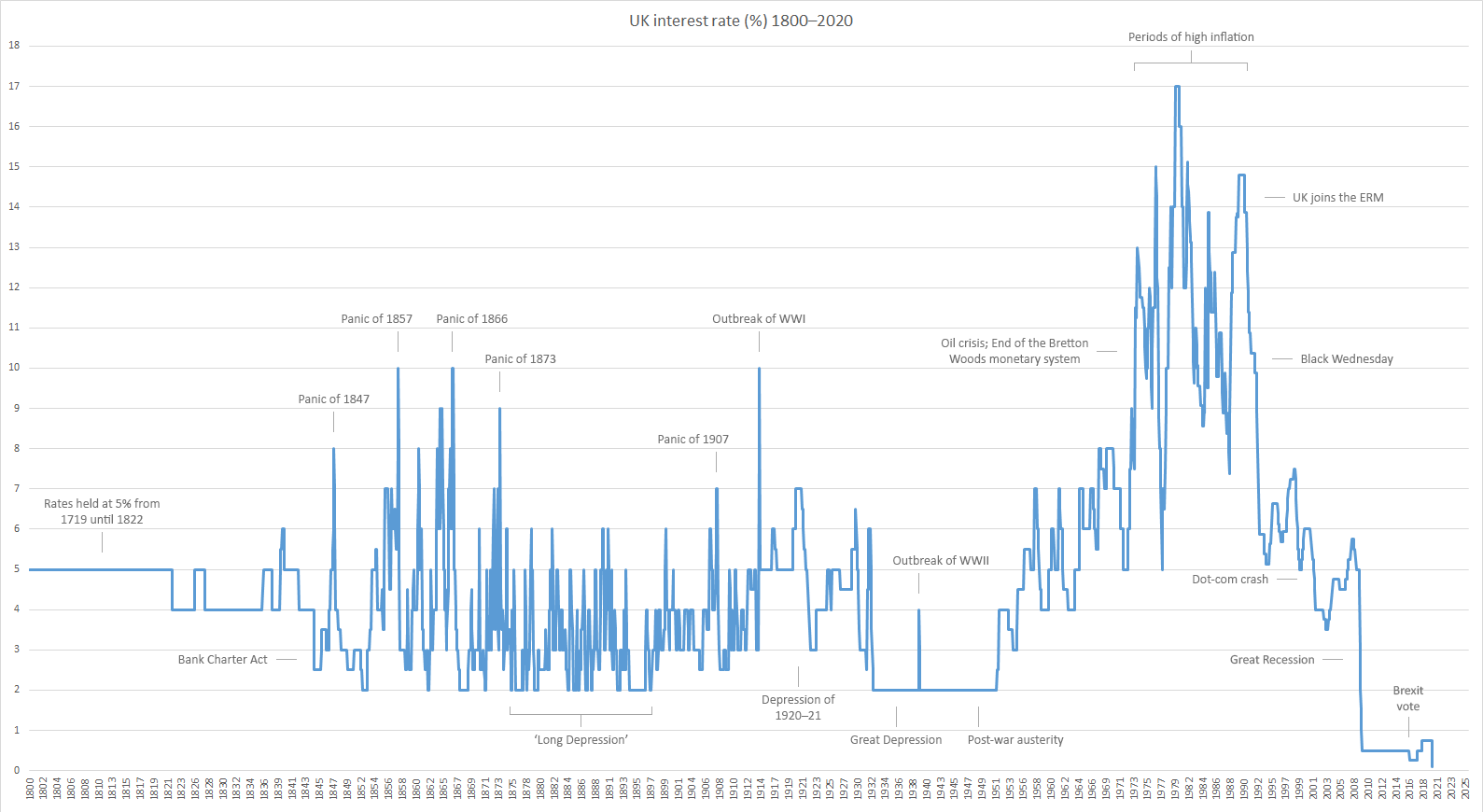

Macroeconomics, the economy, inflation etc. *likely to be very dull*

Comments

-

Sorry, but I mean. Was a rise even contemplated when they were near zero percent!?focuszing723 said: 0

0 -

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches1 -

Should really take the fiscal environment into account when looking at monetary policy.surrey_commuter said:

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches

BoE remit was to keep inflation around 2%. Gov't was embarking on austerity. Rates had to go *really* low. What else you gonna to do stick to the brief?

0 -

I'm not a student of economic history, but I wonder if Covid will end the economic problems of the 2010s in the same way WWII did with the great depression.

It's now possible to get a real return on an index-linked gilt. All remarkably normal.0 -

but we are talking about the subsequent years.rick_chasey said:

Should really take the fiscal environment into account when looking at monetary policy.surrey_commuter said:

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches

BoE remit was to keep inflation around 2%. Gov't was embarking on austerity. Rates had to go *really* low. What else you gonna to do stick to the brief?

We stopped buying bonds at the end of 2021. We stopped reinvesting the proceeds from maturing bonds in February 2022. And we began actively selling bonds in November 20220 -

Sure. inflation was still too low right?surrey_commuter said:

but we are talking about the subsequent years.rick_chasey said:

Should really take the fiscal environment into account when looking at monetary policy.surrey_commuter said:

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches

BoE remit was to keep inflation around 2%. Gov't was embarking on austerity. Rates had to go *really* low. What else you gonna to do stick to the brief?

We stopped buying bonds at the end of 2021. We stopped reinvesting the proceeds from maturing bonds in February 2022. And we began actively selling bonds in November 20220 -

Per my comment above, QE may have been the least bad option immediately post-GFC.rick_chasey said:

Should really take the fiscal environment into account when looking at monetary policy.surrey_commuter said:

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches

BoE remit was to keep inflation around 2%. Gov't was embarking on austerity. Rates had to go *really* low. What else you gonna to do stick to the brief?0 -

But they first upped base rate at the end of 2021rick_chasey said:

Sure. inflation was still too low right?surrey_commuter said:

but we are talking about the subsequent years.rick_chasey said:

Should really take the fiscal environment into account when looking at monetary policy.surrey_commuter said:

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches

BoE remit was to keep inflation around 2%. Gov't was embarking on austerity. Rates had to go *really* low. What else you gonna to do stick to the brief?

We stopped buying bonds at the end of 2021. We stopped reinvesting the proceeds from maturing bonds in February 2022. And we began actively selling bonds in November 2022

my point is that they cotinunued QE for far too long (I blame Brexit)

0 -

Too long or had to do it more because of the feared consequences of brexit?surrey_commuter said:

But they first upped base rate at the end of 2021rick_chasey said:

Sure. inflation was still too low right?surrey_commuter said:

but we are talking about the subsequent years.rick_chasey said:

Should really take the fiscal environment into account when looking at monetary policy.surrey_commuter said:

You should freelance for The Economist as the article echos your thoughtswallace_and_gromit said:

QE may have been the least bad option immediately post-GFC (not so sure myself, but I'm no expert) but in respect of the QE that followed in subsequent years (i.e. the majority of it) recent developments demonstrate that old adages never die:surrey_commuter said:scary stat for the day, it is estimated that the Treasury will have to transfer £275bn to the BofE over the next decade to cover QE losses.

Relatively simple explanation here

To carry out qe, central banks created money in the form of reserves in the banking system and used them to buy long-term bonds, with the intention of lowering their yields. The immediate problem is that as central banks have raised interest rates to fight inflation, they have had to pay out more on those reserves. The coupon payments they receive on the bonds, however, have remained fixed. Selling the bonds to stop the outflow would not help, because they would fetch much less than they cost. Paper losses would crystallise.

- If it sounds too good to be true then it is

- There are no free lunches

BoE remit was to keep inflation around 2%. Gov't was embarking on austerity. Rates had to go *really* low. What else you gonna to do stick to the brief?

We stopped buying bonds at the end of 2021. We stopped reinvesting the proceeds from maturing bonds in February 2022. And we began actively selling bonds in November 2022

my point is that they cotinunued QE for far too long (I blame Brexit)

I agree Brexit narrowed the path to good macroeconomic performance.0 -

According to Statista, the major dollops of QE have been:

Nov 2009 = £200b. Interesting observation is that this was on Labour's watch so nothing to do with auterity.

July 212 = £175b - Austerity-related?

August 2016 = £60b. Presumably Brexit-related though a "small" amount in the context of overall QE, so maybe an un-necessary precaution given that the economy didn't collapse as feared (by some at least).

March 2020 = £210b - Presumably Covid related

June 2020 = £100b - Covid related

Nov 2020 = £150b - Covid related

£895b in total, of which circa £80b has been "Quantitatively Tightened" out. (Difficult to find an exact number.)

https://www.statista.com/statistics/1105570/value-of-quantitative-easing-by-the-bank-of-england-in-the-united-kingdom/0 -

The BoE used to have a graph, but it has disappeared.0

-

Nov 2009 was around the peak of the great recessionwallace_and_gromit said:According to Statista, the major dollops of QE have been:

Nov 2009 = £200b. Interesting observation is that this was on Labour's watch so nothing to do with auterity.

July 212 = £175b - Austerity-related?

August 2016 = £60b. Presumably Brexit-related though a "small" amount in the context of overall QE, so maybe an un-necessary precaution given that the economy didn't collapse as feared (by some at least).

March 2020 = £210b - Presumably Covid related

June 2020 = £100b - Covid related

Nov 2020 = £150b - Covid related

£895b in total, of which circa £80b has been "Quantitatively Tightened" out. (Difficult to find an exact number.)

https://www.statista.com/statistics/1105570/value-of-quantitative-easing-by-the-bank-of-england-in-the-united-kingdom/0 -

Thanks. I thought that went without saying!rick_chasey said:

Nov 2009 was around the peak of the great recessionwallace_and_gromit said:According to Statista, the major dollops of QE have been:

Nov 2009 = £200b. Interesting observation is that this was on Labour's watch so nothing to do with auterity.

July 212 = £175b - Austerity-related?

August 2016 = £60b. Presumably Brexit-related though a "small" amount in the context of overall QE, so maybe an un-necessary precaution given that the economy didn't collapse as feared (by some at least).

March 2020 = £210b - Presumably Covid related

June 2020 = £100b - Covid related

Nov 2020 = £150b - Covid related

£895b in total, of which circa £80b has been "Quantitatively Tightened" out. (Difficult to find an exact number.)

https://www.statista.com/statistics/1105570/value-of-quantitative-easing-by-the-bank-of-england-in-the-united-kingdom/0 -

-

Mind you he's been shorting Tesla for yonks so he's not always film worthy.0

-

NEW YORK, Aug 14 (Reuters) - Michael Burry, the money manager made famous in the book and film "The Big Short," held bearish options against the broad S&P 500 and Nasdaq 100 Index at the end of the second quarter, according to securities fillings released on Monday.https://www.reuters.com/markets/us/burry-famous-big-short-bought-bearish-options-against-sp-nasdaq-100-2023-08-14/

Burry's Scion Asset Management bought put options with a notional value of $739 million against the popular Invesco QQQ Trust ETF (QQQ.O) during the quarter, and separate put options with a notional value of $886 million against the SPDR S&P 500 ETF (SPY.P).0 -

Some investors will see the latest bold move as a warning that the market might get slammed in the coming months as fears of a recession continue to percolate.

The Federal Reserve has been raising interest rates for 17 months now, at times at an extraordinarily aggressive degree. The rate hikes are designed to drive down inflation, but as higher rates trickle through the economy they squelch demand and can lead to a recession and a flagging labor market.

While the labor market has exceeded the expectations of most economists and remained above water, recent jobs reports and other indicators show it is starting to weaken in response to the tightening.

While the stock market has expanded most of this year and the S&P 500 is up more than 17% since the start of 2023, the market has slowed this month and is down slightly since the start of August. The Nasdaq is down by some 2.5% this month.

https://www.washingtonexaminer.com/policy/economy/investor-predicted-housing-crisis-massive-bet-against-stock-market0 -

What’s been his track record since ‘08?focuszing723 said:NEW YORK, Aug 14 (Reuters) - Michael Burry, the money manager made famous in the book and film "The Big Short," held bearish options against the broad S&P 500 and Nasdaq 100 Index at the end of the second quarter, according to securities fillings released on Monday.https://www.reuters.com/markets/us/burry-famous-big-short-bought-bearish-options-against-sp-nasdaq-100-2023-08-14/

Burry's Scion Asset Management bought put options with a notional value of $739 million against the popular Invesco QQQ Trust ETF (QQQ.O) during the quarter, and separate put options with a notional value of $886 million against the SPDR S&P 500 ETF (SPY.P).0 -

focuszing723 said:

Mind you he's been shorting Tesla for yonks so he's not always film worthy.

0 -

That's hell of a position to take though. Eggs n' basket spring to mind.0

-

So in the period 08 to 2021 he averaged about flat, so after fees you were losing money.focuszing723 said:That's hell of a position to take though. Eggs n' basket spring to mind.

S&P500 by contrast was netting you 11% *per year*

Now since 2022 Bury’s made a fortune again, presumably because of that monster short and some other trading which puts returns very high, it still around 3x behind what your s&p500 index tracker was doing since the crash, and they won’t have been charging you 2 and 20.0 -

Inflation was -0.46% in July i.e. deflation. Not uncommon in July, but a sign that inflation is under control.0

-

What about wage increases above the inflation remit target?TheBigBean said:Inflation was -0.46% in July i.e. deflation. Not uncommon in July, but a sign that inflation is under control.

0 -

Last year I had a great joke about inflation. But it's hardly worth it now.

Amos Gill, Edinburgh Festival0 -

A staggering 74% of UK-listed stocks underperformed one-month UK T-bills over twenty-year holding period.

73 per cent of Australian-listed stocks, 77 per cent of Canadian-listed stocks and 86 per cent of Turkish-listed stocks also underperformed their local cash equivalents.

These are some of the surprising results found in two academic studies looking at individual long-term stock returns, with dividends reinvested.

amazing,0 -

UK T-Bills being gilts?

Scottish Widows used to produce a graph of investment returns from 1950 to the present, but stopped some years ago (2015 I think was the last update).

https://www.jjfsltd.com/wp-content/uploads/UK-Financial-History-1950-2015-SW.pdf

Vanguard do a more basic version over 30 years.

https://www.vanguard.co.uk/content/dam/intl/europe/documents/en/vanguard-2022-index-chart-uk-en-end.pdf

0 -

Think I need a graphrick_chasey said:A staggering 74% of UK-listed stocks underperformed one-month UK T-bills over twenty-year holding period.

73 per cent of Australian-listed stocks, 77 per cent of Canadian-listed stocks and 86 per cent of Turkish-listed stocks also underperformed their local cash equivalents.

These are some of the surprising results found in two academic studies looking at individual long-term stock returns, with dividends reinvested.

amazing,- Genesis Croix de Fer

- Dolan Tuono0 -

-

https://www.ft.com/content/caa1139b-e71d-4918-b422-56fdd4f67a3b

If you have an account this article doesn't need a subscription, btw. (which is where the analysis is from)0