Macroeconomics, the economy, inflation etc. *likely to be very dull*

Comments

-

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

0 -

-

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits1 -

Can you explain (to a simpleton) why?rick_chasey said:Well right now the panic is about the pension funds falling over.

We are 80% hedged and margin calls have been less than 10% of fund value so we have just sold bonds to cover it. Is the problem that hedging gets more costly over 80% and/or do they not have liquid assets?0 -

Well exactly.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.0 -

I am at the limits of my knowledge as I am parroting what participants tell me down the phone, but I think it's something to do with the amount of derives used and the size of the collateral required. If you're a long term investor, you don't want gov't actions to force you to liquidate all your liquid positions just to cover the collateral.surrey_commuter said:

Can you explain (to a simpleton) why?rick_chasey said:Well right now the panic is about the pension funds falling over.

We are 80% hedged and margin calls have been less than 10% of fund value so we have just sold bonds to cover it. Is the problem that hedging gets more costly over 80% and/or do they not have liquid assets?

Then you also have to remember the institutional world has made a big pivot away form liquid to private markets (as they "don't need to pay the liquidity premium as [they] are long term investors" as I was told over and over)0 -

Yes, it is the same, but note that central banks always used to do this for shorter term debt in order to set interest rates. Therefore, I imagine the BoE is thinking that a short-term trading position of longer dated bonds isn't the same as longer term QE.surrey_commuter said:

BofE is buying 30 year bonds but is not calling it QETheBigBean said:

I'm not sure what "intervening in the bond market" is a reference to, but QE and the unwinding of it involves buying and selling gilts.surrey_commuter said:@TheBigBean can you tell us if there is a difference between QE and "intervening in the bond market"?

as you know I (like many) thought they were using QE to get new issues away, this just looks like a more blatant versionOpen market operation

From Wikipedia, the free encyclopedia

Jump to navigation

Jump to search

In macroeconomics, an open market operation (OMO) is an activity by a central bank to give (or take) liquidity in its currency to (or from) a bank or a group of banks. The central bank can either buy or sell government bonds (or other financial assets) in the open market (this is where the name was historically derived from) or, in what is now mostly the preferred solution, enter into a repo or secured lending transaction with a commercial bank: the central bank gives the money as a deposit for a defined period and synchronously takes an eligible asset as collateral.

Central banks usually use OMO as the primary means of implementing monetary policy. The usual aim of open market operations is—aside from supplying commercial banks with liquidity and sometimes taking surplus liquidity from commercial banks—to manipulate the short-term interest rate and the supply of base money in an economy, and thus indirectly control the total money supply, in effect expanding money or contracting the money supply. This involves meeting the demand of base money at the target interest rate by buying and selling government securities, or other financial instruments. Monetary targets, such as inflation, interest rates, or exchange rates, are used to guide this implementation.[1][2]

In the post-crisis economy, conventional short-term open market operations have been superseded by major central banks by quantitative easing (QE) programmes. QE are technically similar open-market operations, but entail a pre-commitment of the central bank to conduct purchases to a predefined large volume and for a predefined period of time. Under QE, central banks typically purchase riskier and longer-term securities such as long maturity sovereign bonds and even corporate bonds.0 -

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!0 -

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?0 -

QE was there only hope so I think it rather clever to reintroduce it without reintroducing it.TheBigBean said:

Yes, it is the same, but note that central banks always used to do this for shorter term debt in order to set interest rates. Therefore, I imagine the BoE is thinking that a short-term trading position of longer dated bonds isn't the same as longer term QE.surrey_commuter said:

BofE is buying 30 year bonds but is not calling it QETheBigBean said:

I'm not sure what "intervening in the bond market" is a reference to, but QE and the unwinding of it involves buying and selling gilts.surrey_commuter said:@TheBigBean can you tell us if there is a difference between QE and "intervening in the bond market"?

as you know I (like many) thought they were using QE to get new issues away, this just looks like a more blatant versionOpen market operation

From Wikipedia, the free encyclopedia

Jump to navigation

Jump to search

In macroeconomics, an open market operation (OMO) is an activity by a central bank to give (or take) liquidity in its currency to (or from) a bank or a group of banks. The central bank can either buy or sell government bonds (or other financial assets) in the open market (this is where the name was historically derived from) or, in what is now mostly the preferred solution, enter into a repo or secured lending transaction with a commercial bank: the central bank gives the money as a deposit for a defined period and synchronously takes an eligible asset as collateral.

Central banks usually use OMO as the primary means of implementing monetary policy. The usual aim of open market operations is—aside from supplying commercial banks with liquidity and sometimes taking surplus liquidity from commercial banks—to manipulate the short-term interest rate and the supply of base money in an economy, and thus indirectly control the total money supply, in effect expanding money or contracting the money supply. This involves meeting the demand of base money at the target interest rate by buying and selling government securities, or other financial instruments. Monetary targets, such as inflation, interest rates, or exchange rates, are used to guide this implementation.[1][2]

In the post-crisis economy, conventional short-term open market operations have been superseded by major central banks by quantitative easing (QE) programmes. QE are technically similar open-market operations, but entail a pre-commitment of the central bank to conduct purchases to a predefined large volume and for a predefined period of time. Under QE, central banks typically purchase riskier and longer-term securities such as long maturity sovereign bonds and even corporate bonds.

As our resident expert will you let us know when it is time to panic?0 -

The rest is waffle.0 -

I'm no expert on what a pension is holding, but if it involves long term fixed income, which I expect it does, then it will be worth less. The market for long term swaps is reasonably liquid even if gilts of that length are not traded that much.surrey_commuter said:

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?

I can't explain how pension funds operate other than they seem to pay people lots of management fees.0 -

Time will tell, but for all the screaming interest rates are returning to a more normal level which seems almost promising to me. Index linked gilts now have positive real returns (when they went negative it broke systems). The BoE is unwinding its QE (well sort of). No doubt there will be pain along the way, but after a decade of nothing making sense (negative interest rates etc.) it doesn't quite feel like panic time yet.surrey_commuter said:

QE was there only hope so I think it rather clever to reintroduce it without reintroducing it.TheBigBean said:

Yes, it is the same, but note that central banks always used to do this for shorter term debt in order to set interest rates. Therefore, I imagine the BoE is thinking that a short-term trading position of longer dated bonds isn't the same as longer term QE.surrey_commuter said:

BofE is buying 30 year bonds but is not calling it QETheBigBean said:

I'm not sure what "intervening in the bond market" is a reference to, but QE and the unwinding of it involves buying and selling gilts.surrey_commuter said:@TheBigBean can you tell us if there is a difference between QE and "intervening in the bond market"?

as you know I (like many) thought they were using QE to get new issues away, this just looks like a more blatant versionOpen market operation

From Wikipedia, the free encyclopedia

Jump to navigation

Jump to search

In macroeconomics, an open market operation (OMO) is an activity by a central bank to give (or take) liquidity in its currency to (or from) a bank or a group of banks. The central bank can either buy or sell government bonds (or other financial assets) in the open market (this is where the name was historically derived from) or, in what is now mostly the preferred solution, enter into a repo or secured lending transaction with a commercial bank: the central bank gives the money as a deposit for a defined period and synchronously takes an eligible asset as collateral.

Central banks usually use OMO as the primary means of implementing monetary policy. The usual aim of open market operations is—aside from supplying commercial banks with liquidity and sometimes taking surplus liquidity from commercial banks—to manipulate the short-term interest rate and the supply of base money in an economy, and thus indirectly control the total money supply, in effect expanding money or contracting the money supply. This involves meeting the demand of base money at the target interest rate by buying and selling government securities, or other financial instruments. Monetary targets, such as inflation, interest rates, or exchange rates, are used to guide this implementation.[1][2]

In the post-crisis economy, conventional short-term open market operations have been superseded by major central banks by quantitative easing (QE) programmes. QE are technically similar open-market operations, but entail a pre-commitment of the central bank to conduct purchases to a predefined large volume and for a predefined period of time. Under QE, central banks typically purchase riskier and longer-term securities such as long maturity sovereign bonds and even corporate bonds.

As our resident expert will you let us know when it is time to panic?0 -

But the liabilities are inverse related to the gilt curve so they should have been celebrating not discussing insolvencyTheBigBean said:

I'm no expert on what a pension is holding, but if it involves long term fixed income, which I expert it does, then it will be worth less. The market for long term swaps is reasonably liquid even if gilts of that length are not traded that much.surrey_commuter said:

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?

I can't explain how pension funds operate other than they seem to pay people lots of management fees.0 -

It’s only calmed down because of an emergency BoE intervention.

Underlying issue still remains - market does not believe in the current govt fiscal policy and until that changes, the volatility won’t likely change.0 -

Fair point. I don't know enough about it. Clearly some derivatives are now out of the money, so they need to cash back them in some way, but I'm not really sure what they're hedging to begin with.surrey_commuter said:

But the liabilities are inverse related to the gilt curve so they should have been celebrating not discussing insolvencyTheBigBean said:

I'm no expert on what a pension is holding, but if it involves long term fixed income, which I expert it does, then it will be worth less. The market for long term swaps is reasonably liquid even if gilts of that length are not traded that much.surrey_commuter said:

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?

I can't explain how pension funds operate other than they seem to pay people lots of management fees.0 -

https://12ft.io/proxy?ref=&q=https://www.ft.com/content/038b30c3-f550-4cc0-93ed-9154021d6ee2TheBigBean said:

Fair point. I don't know enough about it. Clearly some derivatives are now out of the money, so they need to cash back them in some way, but I'm not really sure what they're hedging to begin with.surrey_commuter said:

But the liabilities are inverse related to the gilt curve so they should have been celebrating not discussing insolvencyTheBigBean said:

I'm no expert on what a pension is holding, but if it involves long term fixed income, which I expert it does, then it will be worth less. The market for long term swaps is reasonably liquid even if gilts of that length are not traded that much.surrey_commuter said:

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?

I can't explain how pension funds operate other than they seem to pay people lots of management fees.

The link should work for everyone (don't hit the cookies pop up). This explains exactly what's going on in the LDI Market.0 -

It doesn't answer my question about what they are hedging, but I think I've worked that out now.rick_chasey said:

https://12ft.io/proxy?ref=&q=https://www.ft.com/content/038b30c3-f550-4cc0-93ed-9154021d6ee2TheBigBean said:

Fair point. I don't know enough about it. Clearly some derivatives are now out of the money, so they need to cash back them in some way, but I'm not really sure what they're hedging to begin with.surrey_commuter said:

But the liabilities are inverse related to the gilt curve so they should have been celebrating not discussing insolvencyTheBigBean said:

I'm no expert on what a pension is holding, but if it involves long term fixed income, which I expert it does, then it will be worth less. The market for long term swaps is reasonably liquid even if gilts of that length are not traded that much.surrey_commuter said:

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?

I can't explain how pension funds operate other than they seem to pay people lots of management fees.

The link should work for everyone (don't hit the cookies pop up). This explains exactly what's going on in the LDI Market.

So back to SC's question. Pensions take cash in exchange for some long term fixed payments. They could hedge this by buying bonds/gilts, but instead they keep cash which receives floating, then take out a floating to fixed swap, so they have hedged the exposure of the fixed payments to their customers. The swap is very liquid and presumably helps to smooth things out as it can have any profile they like. The problem arises when the swap moves out of the money and requires a load of collateral. I suspect this still wouldn't be a problem if they actually had cash, but many have used debt as well which is now causing problems.

0 -

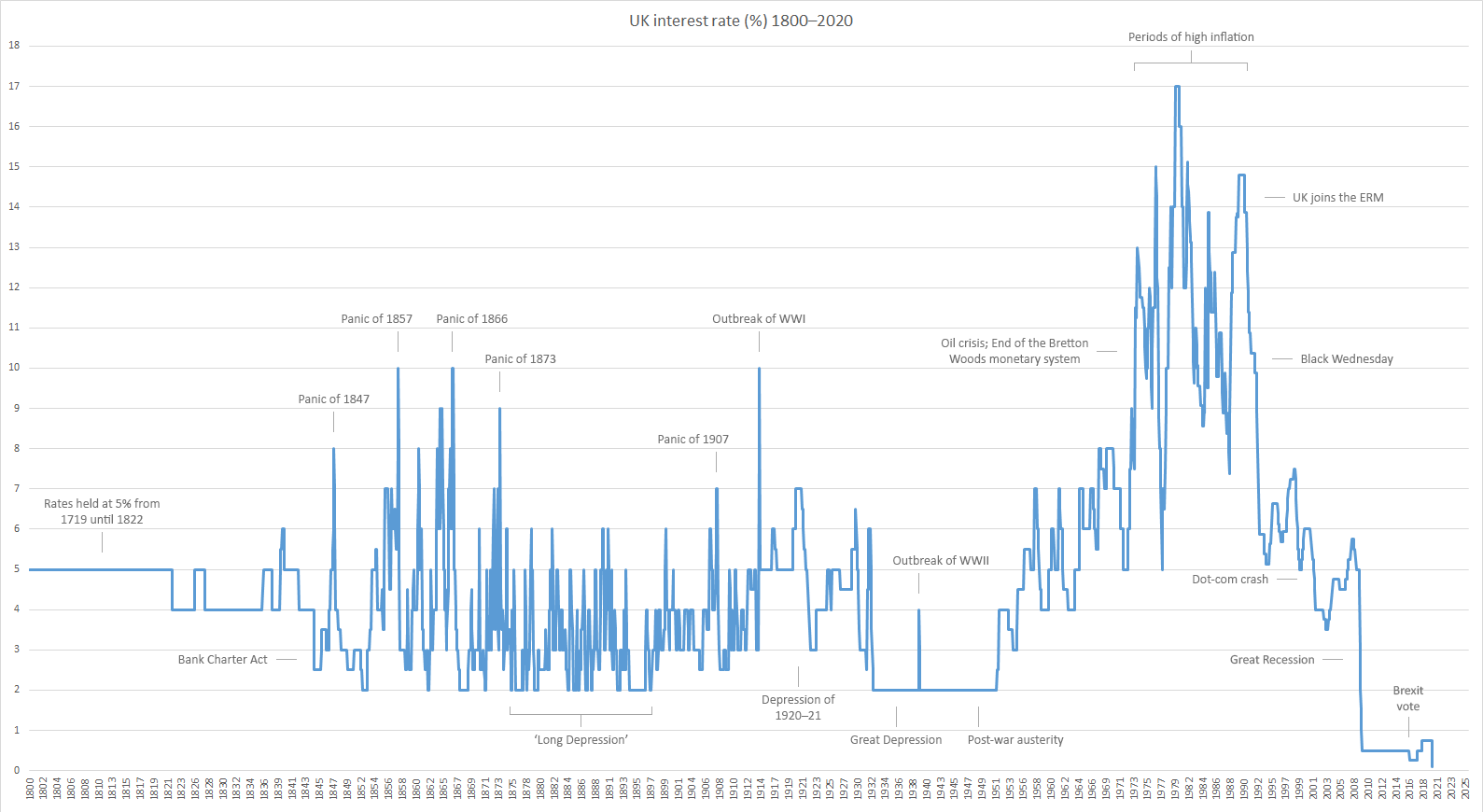

You do realise that if you stick a linear trend line on that graph it suggests that the 'norm' is ever increasing rates... not a horizontal line. Rates are a reaction to other events - not the cause. That's just a graph of how the BoE has reacted to various crises.focuszing723 said:

The rest is waffle.1985 Mercian King of Mercia - work in progress (Hah! Who am I kidding?)

Pinnacle Monzonite

Part of the anti-growth coalition0 -

Waffle0

-

-

I think some have used gilts as collateral which has caused problemsTheBigBean said:

It doesn't answer my question about what they are hedging, but I think I've worked that out now.rick_chasey said:

https://12ft.io/proxy?ref=&q=https://www.ft.com/content/038b30c3-f550-4cc0-93ed-9154021d6ee2TheBigBean said:

Fair point. I don't know enough about it. Clearly some derivatives are now out of the money, so they need to cash back them in some way, but I'm not really sure what they're hedging to begin with.surrey_commuter said:

But the liabilities are inverse related to the gilt curve so they should have been celebrating not discussing insolvencyTheBigBean said:

I'm no expert on what a pension is holding, but if it involves long term fixed income, which I expert it does, then it will be worth less. The market for long term swaps is reasonably liquid even if gilts of that length are not traded that much.surrey_commuter said:

That is still baffling me. I get the value of one of their assets has fallen but rising gilt rates is good for DB pension funds.wallace_and_gromit said:

Given that the BoE action is apparently to stop lots of pension funds going insolvent, one could say that the Kwasi/Truss "Brains Trust" has broken the UK financial system in just 8 working days, given the time off for HM's funeral etc.surrey_commuter said:

lol - having a budget for growth is like "efficiency gains" if it was that easy Govts would have been doing it for decades.wallace_and_gromit said:

But doesn't the impact of such things always fall disproportionately on the less well off? Mrs W&G and I are far from "rich" but having no mortgage and lots of savings, we're not going to be particularly affected by what's coming down the line. We may well downgrade holiday plans a bit, turn the thermostat down and cut back on premium gin etc, but these are the very definition of "First World Problems". Those with more precarious domestic finances are much more exposed to the impacts.kingstongraham said:...the main problems people are facing (and worrying about) are increased mortgage rates, increased inflation etc, all linked to the "sustainability" of the policy.

But in general terms, a very real risk is that what collectively we might gain from growth, we might lose and then some from higher interest rates.

Kwasi/Truss have given us measurable costs and no benefits

Quite the achievement!

TBB - put me out of my misery, they can't have that much 30 year paper so do they have huge derivs positions linked back to a basically illiquid market?

and why bust yourself out meetig margin calls instead of letting the hedge % drop?

I can't explain how pension funds operate other than they seem to pay people lots of management fees.

The link should work for everyone (don't hit the cookies pop up). This explains exactly what's going on in the LDI Market.

So back to SC's question. Pensions take cash in exchange for some long term fixed payments. They could hedge this by buying bonds/gilts, but instead they keep cash which receives floating, then take out a floating to fixed swap, so they have hedged the exposure of the fixed payments to their customers. The swap is very liquid and presumably helps to smooth things out as it can have any profile they like. The problem arises when the swap moves out of the money and requires a load of collateral. I suspect this still wouldn't be a problem if they actually had cash, but many have used debt as well which is now causing problems.0 -

-

Inflation/p1ss taking.

Clothes are still excellent value as well as electronics, cheap as chips and I'm sure there are many other shnazzle too. Reason, massive supply compared to demand, so they have to be competitive.

Which leads me on to some companies just taking the p1ss because they can get away with it. I know that's just capitalism and you have to take the rough with the smooth, but, after Covid (we're all in this together) and the impact of Russia/Ukraine , United Governments should put pressure on the amount of p1ss being taken! Stop the spiral of companies "knock-on" inflationary p1ss.

0 -

Oh, the graph shows a spiral of p1ss.0

-

Here we go.

Officially a “bank of systemic importance” ie too big to fail, so let’s see.

Don’t think it’ll be anywhere as bad as Lehman but hardly good either0 -

How do you "know" this bank is going to collapse? as only a relative handful of people could know this are you sure you should be sharing very market sensitive information?rick_chasey said:

Here we go.

Officially a “bank of systemic importance” ie too big to fail, so let’s see.

Don’t think it’ll be anywhere as bad as Lehman but hardly good either0 -

It is in the public domain. Just as an example...surrey_commuter said:

How do you "know" this bank is going to collapse? as only a relative handful of people could know this are you sure you should be sharing very market sensitive information?rick_chasey said:

Here we go.

Officially a “bank of systemic importance” ie too big to fail, so let’s see.

Don’t think it’ll be anywhere as bad as Lehman but hardly good either

https://www.cnbc.com/2022/10/03/credit-suisse-is-not-about-to-cause-a-lehman-moment-sri-kumar-says.htmlThe above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

If you read even the first 5wordsof that article you would know that CS has not gone bustpblakeney said:

It is in the public domain. Just as an example...surrey_commuter said:

How do you "know" this bank is going to collapse? as only a relative handful of people could know this are you sure you should be sharing very market sensitive information?rick_chasey said:

Here we go.

Officially a “bank of systemic importance” ie too big to fail, so let’s see.

Don’t think it’ll be anywhere as bad as Lehman but hardly good either

https://www.cnbc.com/2022/10/03/credit-suisse-is-not-about-to-cause-a-lehman-moment-sri-kumar-says.html

if it was a foregone conslusion that CS was going to go bust was in the public domain then it would already be bust0 -

? Nobody said it had gone bust. There was a fear that it might.

Even if your only exposure to banking is watching It's a Wonderful Life you would know that all it takes is word of mouth for a run on a bank.

Share price down 9% this morning.The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0