Insuring an uninsurable, irreplaceable bike

Hello road forum, it's been a while.

Looking for insurance advice. My "nice" bike is an ex-Madison Genesis team, very custom, and quite irreplaceable Reynolds 953 steel and Di2 thing. But I have absolutely no idea how I'd go about declaring an insurance value, or more importantly, justifying said value to an insurance company. I legitimately couldn't replace it with anything else that is even close.

Recommendations on specialist insurers, and experiences with insuring other weird/custom/unobtanium bikes would be greatly appreciated.

Comments

-

The fact it is custom or unique makes no difference to an insurer. They are only really going to want to know the value of the bike, with regards what you actually paid for it.

What you would need is an insurer that allows you to declare the full price paid and also factor in any upgrades you made which may have added to the original cost, important when you have a custom bike with no real set rrp, unlike a factory spec bike.

Pedal Cover offer dedicated bike insurance and seem a bit cheaper than some of the other's around.

0 -

I'd so a search for Pedal Cover on this site. I, along with others, used them while they were good. Then they changed conditions. It was a while ago which is why I can't remember why I stopped using them and suggest the search.

The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.1 -

the best way is to use a company such as Chubb for your home insurance. You can add specific high value items, subject to conditions for an agreed value.

they aren’t the cheapest but if you are unfortunate to make a claim, their customer services are top drawer. Highly recommended.

“Give a man a fish and feed him for a day. Teach a man to fish and feed him for a lifetime. Teach a man to cycle and he will realize fishing is stupid and boring”

Desmond Tutu0 -

Ah, that's a shame PB, yes they were a good outfit. I'll have a search through the forum to see what changed.

0 -

Pedal cover are just a broker for other main stream insurers. Their was someone who posted on here I think who was taking them to the ombudsman. They had their bikes stolen, they were locked to someone else’s bike which was locked to an solid fixed object. As their bikes were not locked to the fixed object the insurer refused to pay out.

I wouldn’t use them.

0 -

This is a common method amongst motorbike riders when locking up their bike. It means then can secure their bike to something else (another bike) but you run the risk that the other rider comes and takes their bike away leaving yours unsecured. Most often used when on a group ride and not every bike can get lose to a solid object like a lamp post. Obviously on group rides everyone arrives and leaves at the same time.

As far as it being a method for securing bicycles I would side with the insurer. It's not unreasonable to lift a bicycle to a location where you can lock to a solid object.

0 -

Given what you say then you an only insure it for what you paid for it. Alternatively you could try to get a valuation for the bike from a recognised independent authority (maybe very difficult). I'd guess that's how you would insure a unique piece of jewellery which is valued at more than the weight of gold and carats.

0 -

How does the other rider take their bike away when it's locked to yours?

I also take you up on siding with the insurer. There's often not enough solid objects to secure all the bikes to. If you are locked to another bike which is locked to a solid object that should be good enough, the thief is still going to have to cut a lock or a bike frame before nicking the bike. It is unreasonable to think otherwise. Insurance companies, like most companies, will put profits before being reasonable, as consumers we have to change their point of view by voting with our feet.

0 -

The indisputable fact is that insurance companies can only be judged on how they handle claims.

Before that it is all promises, after that it is too late. Pay close attention to reviews from claimants.

The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

They were all in a group together. So one locked their bike to the solid object and the others locked their bikes to that one. It’s what everyone does on group rides. Given most people are using cafe locks that are made of cheese using an intricate pattern of threading the cables through the bikes makes it harder to steal them.

0 -

You can pass you lock through theirs so either one can unlock it, in fact I seem to remember there being a sticker that you could get to say you were happy for others to do that when I first started riding motorbikes in London.

0 -

You don't lock your bike to the other bike. You lock it to the other bike's lock meaning either can unlock and go. That means the weakest link may not be your premium Platinum rated lock but the cheap chain made from Plasticine bought in Woolworths in 1976. This is why I side with the insurance company. An expensive push bike weighs, typically, less than 10kg so there is no excuse for not finding something solid to lock to, even if it is inconvenient.

0 -

Ah, I see. But you wouldn't do that with a bicycle, you would lock it to the other frame.

I find that it can sometimes be very difficult to find things to lock your bike to, locking to another bike is often the only option at a cafe stop if your'e part of a group.

Things are often even worse at shopping centres. The only official bike parking provision (if they bother to have any at all) is often hidden away and the last place you would want to leave your bike, so you are left trying to find a convenient lamp-post.

0 -

In the case I mentioned I.e. pedal cover they sell themselves on being bike insurance for cyclists and understanding how it is for cyclists. Which is why the guy took them to the ombudsman. As for finding something solid to lock your bike to, that is not always possible if you want to keep your bike in view.

Do you work in the insurance industry by any chance😉

0 -

That simply doesn't work. Bike "A" unlocks and leaves. Bike "B" is now locked to fresh air.

The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

Yup, that's why I mentioned that motorcyclists do it, mostly, when riding in groups so they all arrive/leave at the same time. Also why I side with the insurance company as there is no guarantee of the quality of the thing your bike is locked to even if locked to another bike which is locked to something solid - see my analogy with the 1976, Plasticine Woolworth's chain.

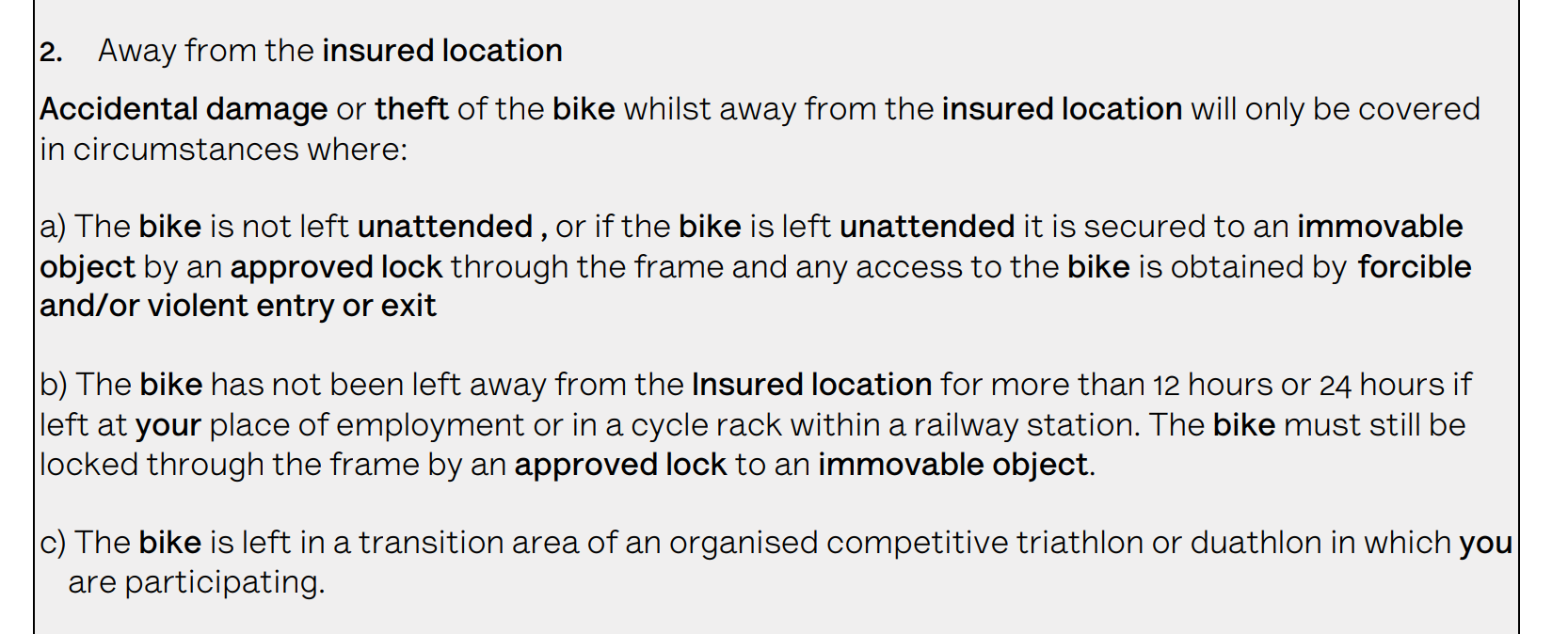

Read the terms and conditions of the insurance policy....... I'll bet good money it mentions the bike being locked to something solid and immovable with a lock and chain which meets certain security standards.

No I don't work for the insurance company but I am lucky enough to love somewhere I can, and do, leave my bike unlocked outside cafes, out of sight and don't worry about it.

0 -

"Read the terms and conditions of the insurance policy....... I'll bet good money it mentions the bike being locked to something solid and immovable with a lock and chain which meets certain security standards."

Mine doesn't. Any that do are prohibitive as I wouldn't carry such a heavy lock. Thanks for the money. 😉

The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

Good luck trying to get bike theft covered on the insurance. It seems they only pay out if you've locked it up so securely you obviously never intend to ride the thing.

Police investigate the total sum of f*ck all of bike thefts, so the insurers aren't going to play nice.

0 -

Pedalsure......

Cycleplan video - https://www.youtube.com/watch?v=NYbk9XtrXK8&t=97s&ab_channel=RipeInsurance

I doubt the Ombudsman will side with the claimant ;-)

0 -

I am not insured through Pedalsure though. I would choose no insurance if the choice was approved lock or no insurance.

PS - This Pedalsure story is an old story and not necessarily relevant, although it did affect my current choice.

The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

That was 2 chosen, partially, at random. I'd expect the vast majority o insurance companies to have those conditions and any that don't will also resist paying out unless you can show "reasonable" precautions against theft. Good luck if you every have to make a claim.

I don't understand why people expect to be covered if they don't take sensible and reasonable precautions. Your car insurance won't cover contents if you leave the door unlocked or the window open. Your house insurance won't cover you if you go out and leave the door unlocked or if there is no evidence of forced entry. Why should bike insurance be any different?

1 -

What an insurer thinks is "reasonable" and what I think are "reasonable" are much further apart when it comes to bikes than homes.

If my bike is in a locked shed, I shouldn't have to then additionally have a ground anchor set in order to D lock it to that too. The insurer disagrees.

Part of the problem is the police do not enforce bike theft. It is practically legal.

0 -

"What an insurer thinks is "reasonable" and what I think are "reasonable" are much further apart when it comes to bikes than homes."

Which is why insurers have comprehensive policies which explicitly state what is required and when you buy that policy you accept those terms. An immovable object and an approved lock are easily understood and not open to interpretation.

Implicit terms in contracts lead to problems, arguments and legal costs. Been there and have the t-shirt.

0 -

Yeah sure. TBH, as I can never meet their standards I don't get it insured.

If I was an underwriter I sure as shit wouldn't want to be underwriting any bikes unless I'm charging a serious premium given the lack of enforcement.

0 -

Me too. My bikes are insured in the garage but as soon as one leaves the house I self insure. Away from my home area I lock it with a cafe lock, Mallorca I use a cafe lock but on a long tour I have a heavy duty cable and Silver quality ABUS padlock.

0 -

When I looked at insuring bicycles, the premium were like 10% of the catalogue prices. And you never pay the full catalogue price, even buying new, and I much prefer buying used.

And of course the insurers wanted you to take precautions, which I find very fair. I think 1) taking precautions, and 2) NOT buying a bicycle insurance, is always the best combo.

BTW, 2 of the 3 bicycles I got stolen in my 50yr would not have been stolen had I taken such reasonable precautions.

1 -

If you have a one-of-a-kind irreplaceable bike, then why the hell are you riding it?

The chances of an accident happening that will destroy the bike are far greater than it being stolen.

You should ask your insurance agent/company about an add-on to homeowners or renters insurance, known as an endorsement, floater, or rider, all 3 of those words are the same thing just depends on what your insurance company calls it, but that will allow you to schedule that particular piece of personal property separate from your regular personal property under an all-risk category. But to do that you will need to get an appraisal from a bicycle shop, get several appraisals, and submit the highest appraisal.

Keep in mind, that all insurance companies will want to know that your bike is locked up at home, and while you're on the road and stop somewhere, and they might have a list of required locks, so you will need to ask what kind of lock do they expect you to have; and they want the bike when at home to be behind locked doors as well, like in a locked garage or inside the house. You'll need to find out all the particulars about insuring your bike because insurance companies will use any excuse not to pay a claim, so make sure you understand what your duties are to secure that bike while at home, riding it, or traveling with it.

0 -

Is your bike really all that unique/irreplaceable? Would it be so hard to get a frame builder (you could probably found out who made yours) to make a 953 frame in MG colours to your spec and then hang DI2 on it. Afaik no one from MG ever won anything that would really interest a collector. I get that we get attached to particular bikes, but insurance companies are not interested in our emotional attachments. Why not just ask a custom builder how much it would cost to build this for you? And then make sure to not leave it anywhere unsafely.

0 -

There's a genesis volare di2 on ebay for £1150.

How much more valuable would yours be?

0