Mortgage fix

Comments

-

because whilst it will fall significantly, it will remain significantly above 2%Dorset_Boy said:From the BBC website:

Bank notes rising wages and inflation in services sector

Daniel Thomas

Reporting from the Bank of England

When the Bank makes decisions to change interest rates, it also provides its reasons for them.

Its Monetary Policy Committee (MPC), which has just set the interest rate, says that inflation in the services sector has remained persistently high, while wages are growing faster than it had predicted back in May.

It added that the impact of “domestic price and wage developments… were likely to take longer to unwind than they did to emerge”.

In a letter to Chancellor Jeremy Hunt, the Bank’s Governor Andrew Bailey said that overall inflation is still set to fall “significantly” during the course of the year as energy prices come down.

But he added that the Bank would continue to monitor inflation closely, and would further tighten monetary policy if there “were evidence of more persistent pressures”.

So if inflation is still set to fall significantly, why did they need to raise the base rate by 0.5%?0 -

I am with FZ that the long term rate is circa 4% so (whilst unwise) I do not see this as panicDorset_Boy said:5% base rate - they've panicked.

0 -

People have been sold this false premise of ZIRP. It's fookin wrong and negligent.surrey_commuter said:

I am with FZ that the long term rate is circa 4% so (whilst unwise) I do not see this as panicDorset_Boy said:5% base rate - they've panicked.

None of this changes the fact Elon Musk is the personification of greatness. Let's get that damn straight and tootin!1 -

focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.0 -

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.0 -

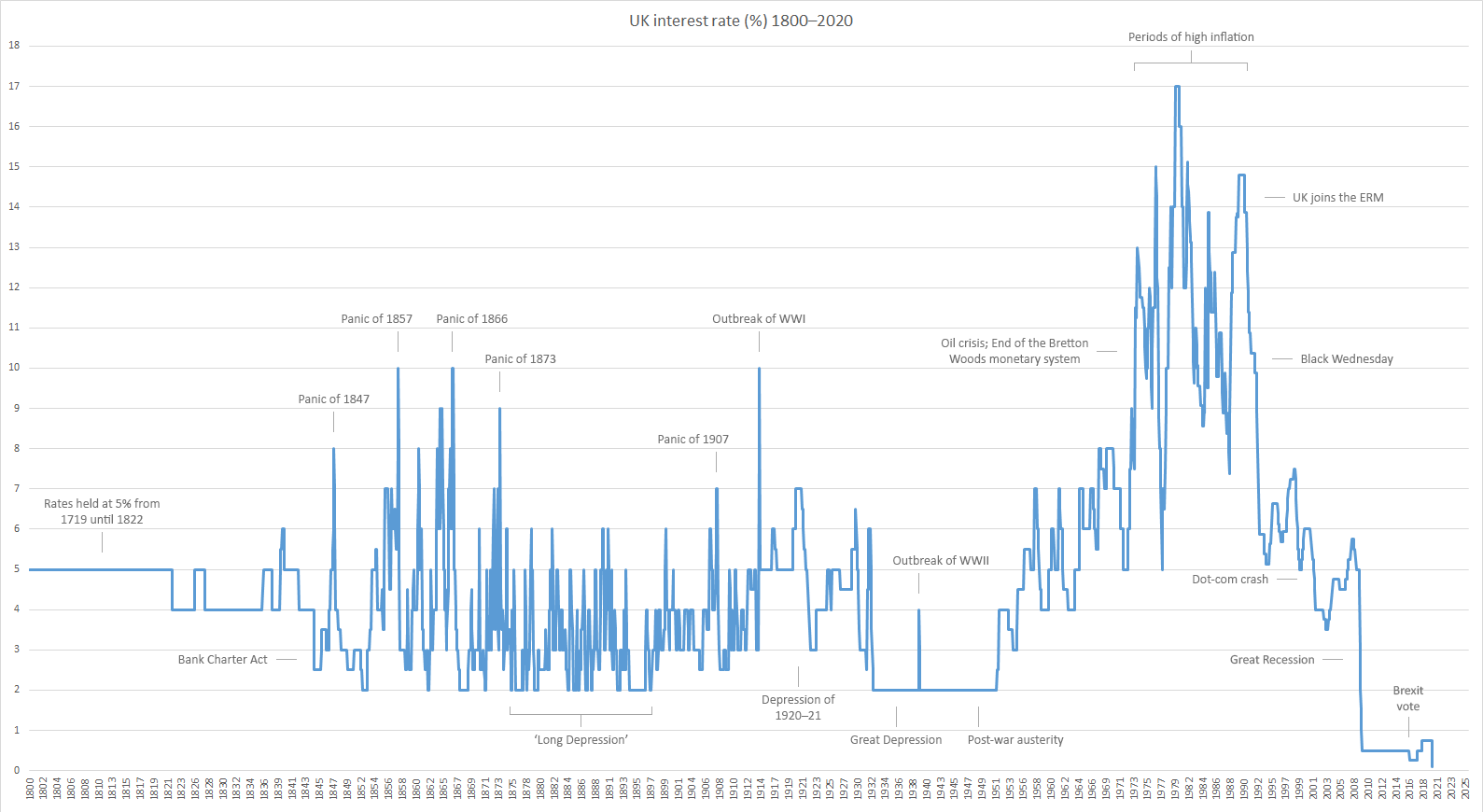

I don't disagree about 4% given since the BoE was formed in 1694, the average base rate is between 4% and 4.5%. 2009-2022 were an anomoly, and whilst money was effectively free, those with debt should have been overpaying.surrey_commuter said:

I am with FZ that the long term rate is circa 4% so (whilst unwise) I do not see this as panicDorset_Boy said:5% base rate - they've panicked.

However, they (the BoE) have not let the rises of the last year work their way through the system yet. That is why they should have paused and not picked with another 0.5% increase.0 -

Isn't it because the core inflation is still going up?Dorset_Boy said:From the BBC website:

Bank notes rising wages and inflation in services sector

Daniel Thomas

Reporting from the Bank of England

When the Bank makes decisions to change interest rates, it also provides its reasons for them.

Its Monetary Policy Committee (MPC), which has just set the interest rate, says that inflation in the services sector has remained persistently high, while wages are growing faster than it had predicted back in May.

It added that the impact of “domestic price and wage developments… were likely to take longer to unwind than they did to emerge”.

In a letter to Chancellor Jeremy Hunt, the Bank’s Governor Andrew Bailey said that overall inflation is still set to fall “significantly” during the course of the year as energy prices come down.

But he added that the Bank would continue to monitor inflation closely, and would further tighten monetary policy if there “were evidence of more persistent pressures”.

So if inflation is still set to fall significantly, why did they need to raise the base rate by 0.5%?0 -

-

Do you have a theory why there even should be a constant 'equilibrium' rate over hundreds of years and wildly different economic circumstances? If we'd been having the same discussion in the 1950s you could make a good argument that the equilibrium rate should be 2%. It's only the peaks of the late 20th century that swing the average back to 4%.surrey_commuter said:

I am with FZ that the long term rate is circa 4% so (whilst unwise) I do not see this as panicDorset_Boy said:5% base rate - they've panicked.

1985 Mercian King of Mercia - work in progress (Hah! Who am I kidding?)

Pinnacle Monzonite

Part of the anti-growth coalition0 -

The problem with ultra low rates is that you have nothing to cut when things start going badly and saves having to invent some bullshit like QE.rjsterry said:

Do you have a theory why there even should be a constant 'equilibrium' rate over hundreds of years and wildly different economic circumstances? If we'd been having the same discussion in the 1950s you could make a good argument that the equilibrium rate should be 2%. It's only the peaks of the late 20th century that swing the average back to 4%.surrey_commuter said:

I am with FZ that the long term rate is circa 4% so (whilst unwise) I do not see this as panicDorset_Boy said:5% base rate - they've panicked.

4% gives you headroom in each direction

2 -

I will preface this by saying my days of studying Economics ceased at A-Level, so I am happy to accept I may well not really have a clue what I am talking about!

However, I have long been of the opinion that (for many involving and complex economic factors), raising interest rates does not actually counter inflation as the BoE seems obsessed with. In fact, constant interest rate rises seem to have the undesired effect of sustained inflation increases (when pursued in unfavorable economic conditions as we are seeing in the UK).

I get the sense that Andrew Bailey and the BoE only really know (or perhaps believe in) the one lever to pull and seem hellbent on pulling it every time (like some knackered one armed bandit in the desperate hope it will eventually pay out).

If anyone can convince me I am wrong I would be glad to listen!0 -

BoE is obsessed by inflation as they are targeted on a rate of 2%. Many people feel they should also have a growth target.MidlandsGrimpeur2 said:I will preface this by saying my days of studying Economics ceased at A-Level, so I am happy to accept I may well not really have a clue what I am talking about!

However, I have long been of the opinion that (for many involving and complex economic factors), raising interest rates does not actually counter inflation as the BoE seems obsessed with. In fact, constant interest rate rises seem to have the undesired effect of sustained inflation increases (when pursued in unfavorable economic conditions as we are seeing in the UK).

I get the sense that Andrew Bailey and the BoE only really know (or perhaps believe in) the one lever to pull and seem hellbent on pulling it every time (like some knackered one armed bandit in the desperate hope it will eventually pay out).

If anyone can convince me I am wrong I would be glad to listen!

Raising base rate will have a downward pull on inflation but is a blunt tool that takes a while for the effects to kick in. Many people feel the increases should have kicked in post covid.0 -

Yeah, and inevitably going to increase. The only question was when.Jezyboy said:

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.

My method copes with both eventualities instead of being tied to one.The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

Still to be convinced prices will fall materially tbh.pblakeney said:

Yeah, and inevitably going to increase. The only question was when.Jezyboy said:

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.

My method copes with both eventualities instead of being tied to one.0 -

Surely that only works when inflation is being driven largely by 'luxury' items though, where people having less money means those things aren't bought as much. A lot of the current inflation is due to basic food shortages and energy costs - People can't just stop eating or using energy.surrey_commuter said:

Raising base rate will have a downward pull on inflation but is a blunt tool that takes a while for the effects to kick in. Many people feel the increases should have kicked in post covid.0 -

Core inflation, which is what worries the BOE, excludes food and energy.whyamihere said:

Surely that only works when inflation is being driven largely by 'luxury' items though, where people having less money means those things aren't bought as much. A lot of the current inflation is due to basic food shortages and energy costs - People can't just stop eating or using energy.surrey_commuter said:

Raising base rate will have a downward pull on inflation but is a blunt tool that takes a while for the effects to kick in. Many people feel the increases should have kicked in post covid.

That's why they differentiate the two.

Don't forget it's not just resi loans, it's also corporate lending.0 -

Supermarkets suggest people are trading down and many people used less energywhyamihere said:

Surely that only works when inflation is being driven largely by 'luxury' items though, where people having less money means those things aren't bought as much. A lot of the current inflation is due to basic food shortages and energy costs - People can't just stop eating or using energy.surrey_commuter said:

Raising base rate will have a downward pull on inflation but is a blunt tool that takes a while for the effects to kick in. Many people feel the increases should have kicked in post covid.0 -

If people used less energy but the price of energy was still high, that doesn't help bring inflation down does it? (as a measure)0

-

Headline inflation sure. That's partly why we're seeing that fall.kingstongraham said:If people used less energy but the price of energy was still high, that doesn't help bring inflation down does it? (as a measure)

Doesn't account for core inflation though.0 -

Dumb Question Time:

If Core inflation excludes things people need why do we care so much?

I would have thought the important one is what people need like food, shelter, etc...? Why does the BofE care more about people affording a TV than food?0 -

If you look at the number of different measures of inflation, you will see it is an inexact science that gives a rough estimate.kingstongraham said:If people used less energy but the price of energy was still high, that doesn't help bring inflation down does it? (as a measure)

0 -

Ja, natürlich, Deutschland hier.Dorset_Boy said:

Am I right in thinking you're in Germany?pep.fermi said:1.91%, took out 2018, fix 20yr.

My investment (or is it savings?) averaged 6% pa, actually my expected average, so good that I made only very minimum overpayment.

20 year fixes have been normal on the continent. will have been really sensible from 2010 to 2022.

Probably not so good now, and weren't attractive pre-2008.

Brits don't like to tie themselves up for any length of time, hence the prevalence of 2 year fixes. Even 5 year fixes haven't been all that popular in comparison.

I was surprised when we took it that even so long fix existed. Germans are still scolded from the hyperinflation they had in between the 2 WWs, unlike you Brits they don't like gambling, they need reassurances.

1 -

I said that it doesn't. If energy is part of the basket and it is high due to external factors, people using less of it doesn't reduce inflation.rick_chasey said:

Headline inflation sure. That's partly why we're seeing that fall.kingstongraham said:If people used less energy but the price of energy was still high, that doesn't help bring inflation down does it? (as a measure)

Doesn't account for core inflation though.0 -

If everyone else in the market is behaving in line with 0% interest rates, then you need to either spend more than you'd like to in your imaginary world where you assume 5% interest, or get much less house.pblakeney said:

Yeah, and inevitably going to increase. The only question was when.Jezyboy said:

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.

My method copes with both eventualities instead of being tied to one.

Tbf we didn't get the biggest mortgage we could, we wanted to keep our repayments around what we were paying for rent, and we fully expected interest rates to rise. What does surprise me is how much they have risen by. I would have thought that we are getting to the point of risking the market, and raising the risk of people getting into negative equity. Although I guess the BoE is only concerned with inflation.0 -

Exactly. Buy what you can afford if/when things go pear shaped. Those of us old enough know that it inevitably will. Pity the young won’t listen.

I’d have liked a nicer house but I didn’t need a nicer house. I view early retirement as a better option than a statement house.

Personal choice and opinion.The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.3 -

Yeah, I’ve been saying since day 1 that increasing interest rates will have minimal effect.rick_chasey said:

Still to be convinced prices will fall materially tbh.pblakeney said:

Yeah, and inevitably going to increase. The only question was when.Jezyboy said:

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.

My method copes with both eventualities instead of being tied to one.

The answer given is that they only have the one tool.The above may be fact, or fiction, I may be serious, I may be jesting.

I am not sure. You have no chance.Veronese68 wrote:PB is the most sensible person on here.0 -

Yeah, there’s an element of victim blaming.Jezyboy said:

If everyone else in the market is behaving in line with 0% interest rates, then you need to either spend more than you'd like to in your imaginary world where you assume 5% interest, or get much less house.pblakeney said:

Yeah, and inevitably going to increase. The only question was when.Jezyboy said:

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.

My method copes with both eventualities instead of being tied to one.

Tbf we didn't get the biggest mortgage we could, we wanted to keep our repayments around what we were paying for rent, and we fully expected interest rates to rise. What does surprise me is how much they have risen by. I would have thought that we are getting to the point of risking the market, and raising the risk of people getting into negative equity. Although I guess the BoE is only concerned with inflation.

The whole market is driven by stupid policies designed to sustain high property prices fuelled ever more by low interest rates.

Trying to get on the ladder you have to play the cards you are dealt which was high prices when everybody else was maxing themselves out.

If you maxed out to get a desirable rather than necessary level of property, you’re part of the problem. Somebody scraping the necessary mortgage to get on the ladder is adding to the problem but given the alternatives has limited choices that aren’t crap.0 -

Energy prices soared so people used 15% less, if they had continued as before then prices would have been higherkingstongraham said:If people used less energy but the price of energy was still high, that doesn't help bring inflation down does it? (as a measure)

0 -

As most of us are in the twilight of our careers so not expecting to double our pay in the next 5 years then I think this is the logical way to look at it. My last mortgage could easily have been £200k bigger but I chose not to for exactly that reason.Jezyboy said:

Meh, it's all very well saying you'd effectively pretend to live with a higher rate, but the housing market was priced with low interest rates in mind.pblakeney said:

Agreed. I'd have done any calculations based on 5% during that period and made surplus payments while lower. Can't afford the house you want? Neither could I.focuszing723 said:focuszing723 said:

Look that fooker in the x and y and tell me that the blissful weren't going to get a right royal kick in the tackle.

This is why it infuriates me that there is even talk that I should help some irresponsible twat to pay his maxed out mortgage.

Why not get sky high returns in a bank or bond you have never heard of as there is no downside as if it goes bust good old SC will bail you out with the money he has on acct at 2% less.2